Banking

Banking Insurance

Insurance Credit Unions

Credit Unions

Professional Services

Professional Services Consulting & Advisory

Consulting & Advisory Legacy Migration

Legacy Migration

Insights

Insights Whitepapers

Whitepapers FAQs

FAQs Brochures

Brochures E-Books

E-Books Glossary

Glossary  Case Studies

Case Studies Events & News

Events & News About Us

About Us Information Security

Information Security FCI Cares

FCI Cares Leadership

Leadership Careers

Careers Partner Program

Partner Program Current Openings

Current Openings

Banks have more customer data than ever before. Every salary credit, card swipe, loan inquiry, deposit renewal, app login, and service request leaves a trace. The hard part is no longer collecting that data – it is acting on it while the moment still matters.

This is where transactional signals come in. Dashboards describe what already happened. Reports summarize past performance. Segments group similar customers together. But growth depends on something faster: reading a customer’s intent as it forms and responding before the opportunity slips away. The bank that turns a single salary credit or a stalled loan application into the right next step is the one that converts, retains, and deepens the relationship.

What transactional signals mean for banks

A transactional signal is any customer event that hints at intent, need, or risk. It is not analytics for its own sake – it is a cue that something should happen next. That next step might be a personalized offer, a retention nudge, a relationship manager task, a service intervention, a document reminder, or a cross-sell journey.

These signals come from the everyday behavior banks already capture: payment behavior, salary credit patterns, deposit activity, loan behavior, and the digital interactions that surround them. Individually, each event is small. Read together and in context, they describe where a customer is in their financial life – and what kind of help would actually be welcome.

This is the heart of transactional intelligence. Banking products are complex, regulated, and lifecycle-driven, and customers rarely know which action to take next. The bank usually does have enough signals to guide them – if it can combine data, interpretation, and orchestration into a single motion.

The banking use case: turning CBS and payment signals into journeys

The clearest use case is straightforward to state and hard to do well: use core banking (CBS) and payment signals to trigger personalized customer journeys across products.

It explains why static, calendar-driven campaigns fall short. A customer moment can appear suddenly and disappear just as fast:

When a bank responds days later with a generic blast, the moment has usually passed. A real-time intelligence layer closes that gap: it recognizes the signal, interprets the context around it, and recommends the next-best action while it is still relevant.

Moving from data to next-best action

A practical customer intelligence model connects four stages.

- Unify the signals. Pull relevant events from core banking, CRM, cards, loans, digital channels, service platforms, campaign tools, and the customer data platform into one view.

- Interpret them. Read those events through rules, models, customer profiles, and behavioral patterns so a raw event becomes a meaningful intent.

- Recommend or trigger an action. Decide the next-best action based on eligibility, intent, value, risk, consent, and channel preference — then act.

- Measure and learn. Track the outcome and feed it back so the next decision is sharper than the last.

This is the difference between customer data and customer action. Data earns its keep only when it helps the bank do something specific, timely, and measurable.

How personalization should work across channels

Good banking personalization is coordinated, not noisy. A customer should not receive a cheerful cross-sell right after raising a complaint. A relationship manager should not call about an action the customer already completed online. A campaign should not keep running after the customer has converted — or declined.

That is why multichannel orchestration matters. SMS, email, WhatsApp, in-app notifications, contact-center prompts, RM tasks, and personalized digital journeys should work as one system, delivering the right message through the right channel at the right moment.

For regulated institutions, personalization must also be trust-aware. Banks need to honor consent, channel preferences, eligibility rules, product suitability, and communication governance. Intelligent engagement is not about sending more messages – it is about making each message more relevant and easier to justify.

From event to journey: practical examples

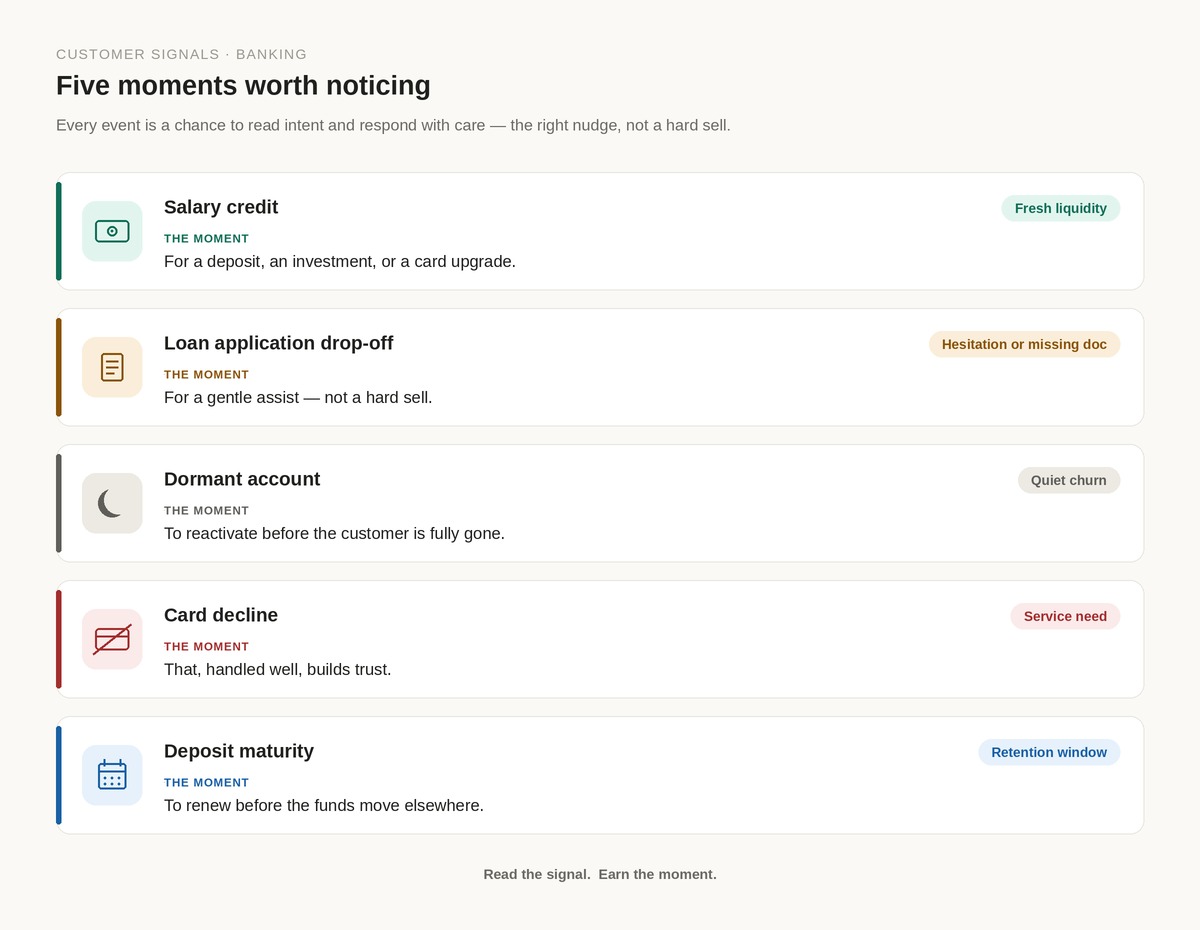

The fastest way to see this work is to map common CBS and payment events to the journeys they should trigger.

| Signal (event) | What it likely means | Next-best action | Suggested channel |

|---|---|---|---|

| Salary credited, balance higher than usual | Fresh liquidity, savings intent | Offer a recurring deposit or short-term investment | App notification + email |

| Loan application started but not completed | Hesitation or missing documents | Send a document checklist and an assisted-completion link | WhatsApp + RM follow-up |

| Fixed deposit nearing maturity | Retention window opening | Pre-approved renewal with a relevant rate | SMS + app |

| No transactions for 90+ days | Early churn risk | Reactivation nudge or a “we miss you” benefit | Email + contact-center |

| Repeated card declines abroad | Service friction, possible limit issue | Proactive support message and limit-review offer | App + SMS |

None of these require new data the bank does not already hold. They require the intelligence to recognize the event and the orchestration to respond consistently.

The business impact for banks

When CBS events become triggers for relevant engagement, the impact shows up across the funnel: higher conversion, more relevant cross-sell, lower drop-off, stronger deposit retention, faster reactivation of dormant customers, better RM productivity, less wasted campaign spend, and clearer ROI attribution.

The underlying value of transactional intelligence is timing. If a customer is ready to borrow, save, invest, renew, reactivate, or finish a journey, the bank should be able to respond with context – before that intent becomes a missed opportunity.

KPIs banks should track

To know whether this is working, track a focused set of outcomes:

- Conversion rate and click-through rate

- Journey completion rate and product uptake

- Offer acceptance rate

- Dormant-customer reactivation and churn reduction

- RM contact productivity

- Campaign cost per conversion and incremental revenue

- Consent adherence and channel-preference performance

A mature intelligence layer also learns from what did not work. Ignored messages, repeated drop-offs, channel opt-outs, and failed conversions all sharpen the next decision. That closed loop is what makes each campaign a little smarter than the one before it.

How VARTASense supports the journey

VARTASense is an AI-driven customer intelligence and engagement layer built for exactly this shift – from broad segmentation and static campaigns toward real-time, persona-aware, and measurable engagement.

Its focus is converting customer signals into action: micro-segmentation, next-best-action recommendations, persona-aware nudges, multichannel orchestration, consent-first delivery, CRM and core banking integration, closed-loop learning, and ROI visibility. In practice, that means the deposit, loan, and card journeys above stop being one-off ideas and become repeatable, governed, and trackable motions.

Conclusion

Banking growth is no longer only about acquiring more customers or running more campaigns. It is about understanding the customers a bank already has and acting at the right moment with relevance.

AI-driven customer intelligence closes the gap between what a bank knows and what it does. With VARTASense, banks can move from dashboards to decisions, from segments to personalized journeys, and from campaign activity to measurable growth.

Turn transactional signals into journeys with VARTASense.

FAQs

What do transactional signals mean in banking?

Why do transactional signals matter for transactional intelligence?

How does VARTASense help with this use case?